When Missing the Best Doesnt Matter

Whenever individual investors begin getting nervous about staying invested in equities, it seems the media trots out one of the oldest arguments against active management what if you miss the best days of the market? One of the latest such arguments against using active management taps into a 2021 study by Bank of America on missing the best and worst days of the market.

CNBCs analysis of the data states: Looking at data going back to 1930, the firm found that if an investor sat out the S&P 500's 10 best days per decade, total returns would be significantly lower than the return for investors who waited it out. And the markets best days typically follow the largest drops, meaning panic selling can lead to missed opportunities on the upside.

Bank of America is a curious voice for passive management since its own marketing boasts of a tried and true market indicator, which provided a powerful contrarian buy signal in March of 2022. By December of 2022, Bank of America's Research Investment Committee was advising It won't be time to buy into stocks until after the Fed makes its last rate hike.

Perhaps the contradiction between CNBCs analysis of the chart and Bank of Americas support of active management can be explained by taking a second look at the studys results.

Yes, missing the best days of the market significantly reduces return and yes, the best days and worst days often occur very closely together. But the outsized benefit of missing the worst days, makes it clearly appear worth the effort of trying to do so. Even more interesting is the fact that one doesnt need the best or the worst days to outperform a buy-and-hold position. Out of 10 decades, missing both the best and worst days underperforms a buy-and-hold position in only two decades the 1930s and the 1970s, according to the study.

The best and worst days of the market typically occur in highly volatile market periods, when market risk is at its highest.Active management isnt about making 100% in or out of the market decisions. It means adjusting portfolio positions in response to perceived market risk to limit the potential for losses or capitalize on healthy upswings. Any time we can reduce losses in down markets, the portfolio has more to invest in rising markets. Thats when active management has the ability to make a difference.

SOURCES:

* This chart shows why investors should never try to time the stock market, CNBC, published Wed, Mar 24 2021 12:15 PM EDT Updated Wed, Mar 24 20212:18 PM EDT.

** Bank of Americas reliable market-timing tool has been triggered, signaling short rally ahead, CNBC.

published Fri, Mar 25 2022 10:22 AM EDT.

** Heres how to invest in the stock market next year, according to Bank of America, by Phil Rosen, Dec 8, 2022, 4:15 AM MST BusinessInsider.com

TOP

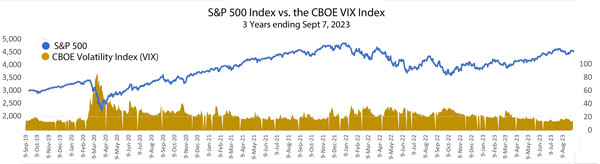

Volatility Increases in Uncertain Markets

One of the more useful tools for measuring investor uncertainty is the Chicago Board of Options Exchange VIX index. The VIX Index is designed to produce a measure of constant, 30-day expected volatility of the U.S. stock market, derived from real-time, mid-quote prices of S&P 500® Index call and put options. In declining markets, volatility tends to increase as shown by the VIX index versus the S&P 500 over the past three years.

The problem with market declines is that no one knows how much will be lost, how long the fall will last, or how much time it will take to recover. It doesnt matter how good a portfolio might potentially perform if the investor is unable to stay the course during bear markets.

Unfortunately, real people tend to sell when the pain is the greatest and then hesitate to re-enter the market until they have missed too many good days. Its not that they are stupid. Its that they dont have sufficient funds that they can afford to wait a decade to recover. Its easy to sit out a market crash with a $1 billion portfolio and no immediate need for all $1 billion. Watching a $500,000 retirement portfolio whittled down to $300,000 can be devastating.

This is where the results of missing the best and worst market days are so important. While no investment manager will ever miss just the best and worst days, by reducing portfolio volatility and enabling investors to stay with their investment plan for the long term, the potential for investment success is enhanced.

TOP

Threats to Your Financial Security Continue to Escalate

It has never been more important to be wary of any unfamiliar contacts by email, text, phone, mail and social media inquiring about your financial accounts.

The world is now four months into what may well be the largest digital data theft ever - the MoveIt data breach. As of late August, up to 600 organizations have been identified as victims with the loss of information impacting more than 40 million customers. Many security experts fear that is just the start. Ransomeware threats have been issued to companies, healthcare providers, government entities, financial services providers, pension fund administrators and more with the threat that failure to pay up will result in the release of customer and client personal data on the dark net.

MOVEit is a file transfer program owned by Progress Software and used on an international scale. A wide range of organizations in public and private sectors worldwide used the program to move sensitive personal data. In May 2023, users became aware that a hacker group called CL0P had gained access to MOVEit and malware was used to steal sensitive information from databases. Some computer security analysts have expressed concerns that the group may have initially gained access up to two years ago.

Was your data among the hacked databases? Who knows? You may receive notices from companies acknowledging that your data was stolen, but others may still be unaware. If your data makes it onto the dark web, it could be purchased for as little as $1 and turned against you.

What you need to do now is dramatically lower your trust level and up your account monitoring.

One of the most effective tools of data theft are direct attacks, where ID thieves use the details they gain from hackers to trick victims into revealing more details that give them access to financial accounts and credit cards. This could be a phone call, email, letter, text message or other messaging tool providing just enough details about your account that it appears a genuine contact from the company. NEVER respond to contacts you did not initiate. Contact the company directly. Do not use contact information provided by the caller.

If you are notified that your data has been compromised:

- Freeze your credit to prevent accounts being opened in your name. Contact the three major credit bureaus, Experian, Transunion and Equifax and ask them to lock your account. Caution: This will also prevent you from applying for credit. You'll have to "thaw" your credit file first.

- Initiate a fraud alert with each of the three credit bureaus. This typically lasts just a year, but you can extend it to seven years.

- Request a free copy of your credit report at AnnualCreditReport.com and check for any accounts you do not recognize. Close those you do not use.

- Change important passwords and login information and use multifactor authentication to access accounts.

- Set account alerts on financial accounts! This includes banks, credit unions, credit cards, investment accounts and insurance companies.

- Monitor your accounts and credit. Keep an eye on your bank accounts and credit cards for any activity you don't recognize. If you receive charges in your name that aren't yours, contact the lender immediately to dispute the items.

You may receive a notice from a company that held your data offering to provide ID theft monitoring. It may be a good offer to accept, but dont use contact information provided in the letter. Contact the company directly to make certain it is a genuine offer and not another scam.

There is a war underway and you dont want to be collateral damage. If you have older relatives, this may also be the time to take steps to help prevent them from falling victim to identity theft.

TOP

Does Your State Owe You Money?

Is there a chance you have misplaced money by forgetting about an old account or a safe deposit box? Did you have funds in a failed bank and have given up trying to reclaim them? Or, perhaps more likely, are you an executor for a deceased person and wondering if they had lost track of a bank account, certificate of deposit, investment account, or safe deposit box?

If the property remained unclaimed and is classified as abandoned under your states statutes, the bank may be required to transfer the contents of an account or the safe deposit box to the state treasurer or state unclaimed-property office in a process called escheat.

To find out if an account balance or property from a safe deposit box was sent to the state treasurer, you will need to contact your applicable state treasurer/unclaimed-property office. The Federal Deposit Insurance Corp. (FDIC) offers some useful information on how the process works and web addresses for the appropriate state agencies. Good luck!

https://closedbanks.fdic.gov/funds/

https://www.fdic.gov/resources/resolutions/bank-failures/failed-bank-list/unclaimed-property-states.html

TOP

Catch-up Contributions to 401(k) Plans Continue to Be Tax Deductible in 2024 and 2025

Good news for age 50-and-over participants in 401(k), 403(b) or governmental 457(b) plans who make catch-up contributions.

Section 603 of the Secure 2.0 Act, enacted in December 2022, required employees who participate in and whose prior-year Social Security wages exceeded $145,000, to make after-tax catch-up contributions to a Roth account starting in 2024.

This past August, the Internal Revenue Service granted an administrative transition period that extends until 2026 to the new requirement that any catch-up contributions made by higher income participants in 401(k) and similar retirement plans must be designated as after-tax Roth contributions. 401(k), 403(b) or governmental 457(b) plan participants can continue to make tax-deductible catch-up contributions up to $7,500 to their retirement accounts in 2024 and 2025.

2023 catch-up contributions to a 401(k) can still be made on a tax-deductible basis through the April 15, 2024 deadline.

The administrative transition period, the IRS explained, will help taxpayers transition smoothly to the new Roth catch-up requirement and is designed to facilitate an orderly transition for compliance with that requirement.

The IRS notice also clarifies that the SECURE 2.0 Act does not prohibit plans from permitting catch-up contributions, so plan participants who are age 50 and over can still make catch-up contributions after 2023.

By making catch-up contributions with pre-tax money, an individual in a 35% bracket would receive a $2,625 tax deduction for a $7,500 catch-up contribution, while someone in the 22% bracket would deduct $1,650.

That deduction will disappear in 2026, however, there are benefits to putting money in a Roth, where it can be withdrawn tax-free.

TOP

Stop Procrastinating and Take Action

Its always easy to second guess decisions we should have made that would have left us wealthier today. We should have bought that empty lot, Uncle Joes gold coins, a rental property for the kids during college, Microsoft or Apple stock in the 1980s, and so much more.

All too often procrastination played a role in our failure to act. We may have been waiting for prices to pull back, for the market to turn up, or for an expected bonus to arrive. But the biggest reason people procrastinate when it comes to making financial decisions is the fear that they will be wrong.

Procrastination is the practice of avoiding, delaying, or postponing actions even if delaying action could have negative or undesirable consequences.

When it comes to investing, three basic fears tend to feed procrastination:

- Youre afraid of losing money.

- You dont think you know enough to evaluate the investment or the financial advice you receive.

- You experience anxiety, fear, or doubt about money-related matters or about your ability to manage your money.

Any one of those fears can be overwhelming. Put all three together and they can paralyze your ability to act. If you let that happen, you endanger your ability to ever achieve financial security.

Life has risks. Investing has risks. There is always the chance that you will have a bad investment and lose money. But not investing simply guarantees that you lose the buying power of your money to inflation. Achieving financial security requires that we put our money to work earning money at a rate that outpaces inflation and creates value over time.

In 2013, legendary investor Warren Buffett offered a very simple do-it-yourself investment plan for individuals. Dollar-cost average by making regular investments monthly or annually - split 90% between a S&P 500 ETF and 10% short-term Treasury bonds. The S&P 500 allocation provides market-based returns; Treasury bonds provide a cash buffer for holding on during down markets and recovery.

Based on historical returns, Buffetts investment plan works given sufficient time, i.e. 15-30 years. The catch is that there will be periods of significant downturns and losses. Few people have the fortitude to continue investing during major market downturns such as 2000-2002, when the S&P 500 lost more than 50% of its value and took 10 years to return to breakeven.

Thats where investment advisors earn their fees. Our job is to help your money make money. Not every investment will be profitable. But if we can help you stay invested for the long term, make regular contributions to your portfolio and avoid procrastinating when it comes to financial decisions, the odds of your success increase significantly. We have also made a profession of following financial markets, studying investment strategies that have succeeded and working with clients to design portfolios that meet their risk tolerance and financial situation.

If procrastination is undercutting your ability to build financial security, talk with your financial advisor and put together a plan to overcome your hesitations. Your future could well depend upon doing so.

TOP