Time In the Market is Critical for Investment Success

Investing is about managing the risks that will substantially reduce your ability to stay in the game long enough to win.

Lance Roberts

The first reality of investing is that financial markets are volatile.

Since 1950, there have been 11 bear markets when the S&P 500 Index lost 20% or more of its value. It took 13 years for the index to recover from the consecutive bear markets that began in March 2000 and October 2007 and begin making gains again.

The second reality is that it is hard to outperform the buy-and-hold return of the S&P 500 index.

Investors have typically been rewarded over the long term for their willingness to accept the risk and volatility of the market by performance that few investment managers exceed.

So why not just invest in a S&P 500 index fund and walk away for the next 20-30 years? After all, Warren Buffetts recommended portfolio for individual investors is 90% in a S&P 500 index fund and 10% in a low-cost, short-term U.S. government bond index fund held for the long term.

The problem is that no one knows how much will be lost in a market decline, how long the decline will last or how much time it will take to recover. Every bear market takes place in unique circumstances. There are no guarantees that the magnitude of the next decline or time to recover will reflect past downturns. Nor can there be any assurance that ones portfolio will have recovered by the time the investor needs the funds.

The memory of the crash of 2000 when an estimated $8 trillion of wealth was lost is still very fresh in investors memories. The market had barely returned to its 2000 highs in 2007 when a second jolt sent it down 42% before the end of 2008. Most recent was the Coronavirus Crash, 33 devastating days from Feb. 12 to March 23, 2020 when the S&P 500 fell 34%.

It doesnt matter how great a portfolio might perform over the long run if the investor is unable to stay the course during bear markets. Real people tend to sell when markets collapse and then hesitate to re-enter the market until they have missed much of the recovery. Its not that they are stupid. Its that they dont have sufficient funds that they can afford to wait a decade to recover.

Its easy to sit out a market crash with a $1 billion diversified portfolio and no immediate need for the full $1 billion. Watching a $500,000 retirement portfolio whittled down to $300,000 can be devastating. There are no guarantees that the portfolio will recover in time to meet your retirement needs. If you need to withdraw from the portfolio to meet living costs following a bear market loss, in many prior market declines you would never have recovered from the loss and run out of money much too soon.

The quote at the start of this article summarizes Investing in a nutshell. The investor has to stay in the game long enough to win. That means managing the risk of major portfolio drawdowns and making certain the investor has the funds they need, when they need them.

There is a cost to limiting risk. Less risk typically means less opportunity for gains over the long run. Over the short run, limiting risk may outperform market return. Miss a substantial part of a bear market, and you have more money to invest when the market turns back up. That may be enough to counteract the cost of missing an early part of the rebound.

For your investment portfolio to succeed, you have to be in for the long run. That requires an investment approach that limits risk to a level that makes sense for your financial situation. While there can never be a guarantee that an investment approach will be successful, buy-and-hold investing comes with the reality that your portfolio can lose substantial value in a market downturn with no guarantees of how long it will take to recover or if you will recover.

If you are uneasy about your investments in todays tumultuous environment, schedule an appointment with your investment advisor and make certain you understand your risk exposure, how your advisor will strive to protect your portfolio in the event of a market decline and if you have the confidence to stay in the game long enough to win.

All investments and investment strategies have the potential for loss as well as gain. Past performance is no guarantee of future returns. Information in this article is not intended as investment advice, but rather to provide a better understanding of investment principles.

TOP

Updating Your Retirement Plan Beneficiaries Matters More Than Ever

Its time to update and rethink your retirement plan beneficiaries.

Given the last year and a half, you want to make certain your designated beneficiaries are still alive and that there have not been changes in marital status or new babies that you need to take into consideration. Equally important, you need to realize the rules for withdrawing funds from an inherited IRA have changed for non-spouse beneficiaries.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 eliminated the ability to stretch an inherited IRA over the lifetime of the beneficiary. Non-spouse beneficiaries of inherited IRAs are now required to withdraw and pay taxes on distributions from inherited retirement accounts within 10 years. Failure to empty the account in 10 years will result in an IRS 50% penalty on the amount remaining in the account.

There are exceptions to the 10-year rule. In addition to a spouse, an Eligible Designated Beneficiary (EDB) can withdraw funds from an inherited IRA over an extended period. An EDB includes a minor child (but not grandchild), a person with special needs or a chronic illness, and beneficiaries who are not more than 10 years younger than the IRA owner. Once a minor child reaches the age of majority - 18 or 26, the clock starts running and the individual has 10 years to withdraw the remaining balance.

Heirs of IRA owners who died in 2019 or before are grandfathered into the stretch rule and are not required to meet the 10-year withdrawal deadline.

Up until passage of the SECURE Act, many IRA holders viewed passing retirement assets onto children, grandchildren and unrelated heirs as a way to provide them with retirement security. Beneficiaries were able to stretch payments over their lifetimes, allowing assets to continue to grow tax deferred. At withdrawal, heirs were responsible for paying taxes on withdrawn funds at their personal tax rates. That is no longer possible for all beneficiaries given the 10-year requirement.

Perhaps the biggest question that arises with the 10-year rule is whether or not it makes more sense to spend retirement account assets first and leave non-retirement assets to ones heirs. In the case of smaller estates, non-retirement assets are likely to pass on to heirs tax-free. While the Biden Administration has expressed the desire to eliminate mark to market on estate assets potentially resulting in capital gains taxes on inherited assets, capital gains tax rates have traditionally been lower than personal tax rates.

With an inherited IRA, the need to withdraw a substantial IRA balance in 10 years could occur during the heirs highest earning years. If withdrawals push the beneficiary into a higher tax bracket, the rate would apply to personal income across the board. Its also possible that the increase in taxable income could make it more difficult for student beneficiaries to qualify for financial aid for college.

You might want to designate as a beneficiary for your traditional retirement account someone who qualifies as an EDB or is in a lower income-tax bracket.

Converting a traditional IRA to a Roth IRA, could allow the retirement account holder to take advantage of the current low income-tax rates (compared to proposed future rates). While Roth IRAs are still subject to the 10-year distribution requirement for non-EDBs, distributions arent counted as taxable income when the beneficiary withdraws the funds. You are required to pay personal income tax on amounts converted to a Roth IRA the year in which you convert.

If your priority is to leave the maximum after-tax benefit to your heirs, discuss the new requirement for 10-year distribution of inherited IRA account assets with your estate planner or financial advisor. They can help you understand the pros and cons of different approaches to the beneficiary puzzle.

The preceding information is provided for educational purposes only and is not intended as financial or estate planning advice. Always consult a qualified financial advisor before making any changes in your estate plans or retirement accounts.

TOP

ADVICE FOR GEN Y & Z

Rule 1: Pay Yourself First

Pay yourself first means taking a regular amount from every income payment or even unemployment check and setting It aside in a savings account. The sooner you get in the habit of paying yourself first, the easier it is to increase those payments as your income increases. Receive a bonus? Put a portion in your savings account. Inherit money? Set some aside for your future.

Money begets money when properly invested. If you never set money aside, you never have a chance to experience the effect of compounding, where you earn interest on interest and the growth of your savings accelerates. Without savings, you never have the funds to invest and take advantage of the growth of a business. Without access to savings in an emergency, a small disaster can snowball into a major catastrophe.

Pay yourself first. Its your financial future at stake.

TOP

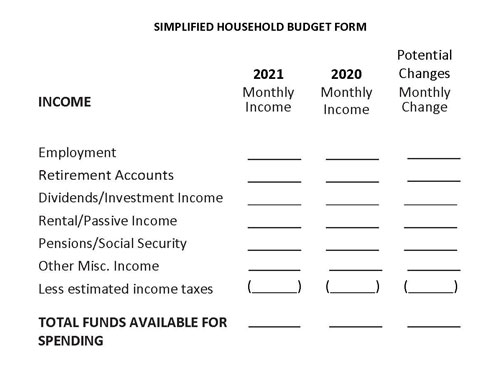

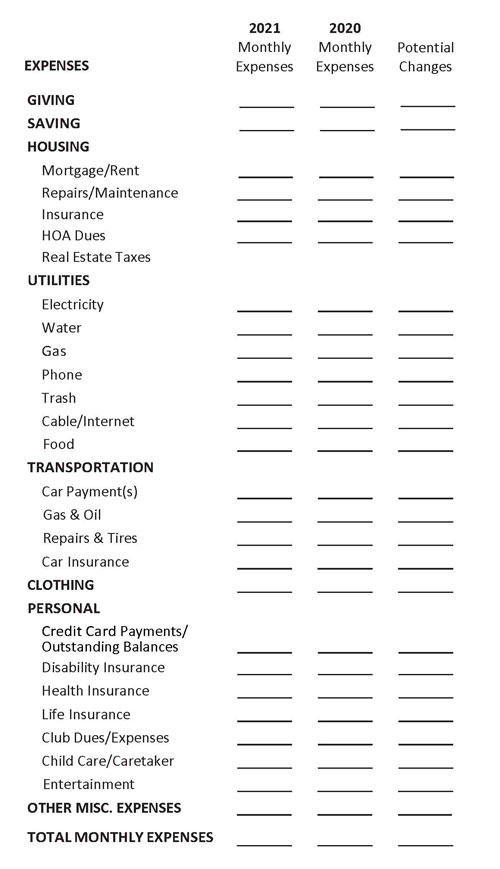

Like it or not, inflation is with us. It may be transitory, but more and more, inflation looks like a multi-year companion. And when it comes to the cost of living, what goes up rarely comes down again. The trick is to learn how to live with inflation without having it destroy your lifestyle.

Living with inflation starts with the one word almost everyone dislikes BUDGET. Even if you think you have plenty of funds to withstand the impact of inflation on your life, unless you run the numbers, you are just guessing.

To plan for inflation, particularly if you are retired or nearing retirement, you need to know how much income or potential income you have; how much is currently spent on essential costs, such as utilities, insurance, mortgage, taxes, etc.; what you might need in the future; where you can generate additional funds to pay essential costs, and where you might be able to economize. To grasp the impact of inflation, its helpful to know how these numbers compare to a year ago.

Where do you find the information you need? Bank statements and credit cards will provide the bulk of the data. Many credit card companies provide end-of-year summaries showing where you spent your money, as do some banks. Its going to take some time to pull everything together, but the better the information, the better your understanding of where your money comes from and goes. Estimates are always better than nothing, but you might be surprised to find out what the actual numbers are.

In addition to helping you look for ways to live with inflation, putting together a budget gives you a sense of control over your finances which can lower your stress and worries. And, your budget gives your financial advisor a way to help you understand your options.

Once you have at least a preliminary outline of where you are with respect to your income versus expenses, you should have a pretty good idea of how inflation is affecting you and could impact your future. If you are comfortable with the numbers and your ability to live with inflation, you now have a reason to feel that way.

If the numbers make you nervous, call and set an appointment to go over your financial situation with us. An outside viewpoint can be invaluable. Given the information you now have, combined with our awareness of your investment portfolio, we can help look at your options and possible solutions.

TOP