Are Minimal Returns in the Future for Equities?

In mid August, all three major indexes S&P 500, Dow Jones Industrials and the Nasdaq - simultaneously hit new highs for the second time in a week. With primarily good news in recent market performance, why are an increasing number of big name firms and analysts projecting minimal returns for the stock market over the next five to ten years?

At the root of their concerns is that the current market is speculation driven. With interest rates at record lows, investors are looking to riskier assets for return on their investments, fueling demand for equities, particularly equities with dividends. That demand drove stocks to a Shiller PE ratio in excess of 27 in August. Over the last 10 years, the ratio average has been 15, putting stock valuations 71% higher than their 10-year average. For stocks to move higher beyond the impact of pure speculation according to fundamental valuation, they have to increase real revenues and earnings.

The source of those increased earnings is the big concern. The U.S. economy has failed to achieve significant growth momentum for 10 years and the recent trend is not encouraging.

Source: U.S. Bureau of Economic Analysis.

Over 70% of the current U.S. GDP is from consumer spending, which is another concern. While unemployment is below 6% nationally, the underemployment rate is closer to 14.6%, wages are stagnant, personal debt levels are high, and one in seven Americans are on food stamps. A number of moves are underway to increase minimum wage levels across the U.S., however, increasing labor costs without corresponding increases in productivity has the potential to depress corporate profits, putting downward pressure on earnings per share.

The largest companies in the S&P 500 report considerable income from overseas sales, but with global GDP in the doldrums as well, these sales may not be enough to make up for a sluggish U.S. domestic market. The Conference Board outlook for global economic growth is a relatively modest 2.4% in 2016 and 2.7% in 2017. This compares to the International Monetary Funds slightly more optimistic projections of 3.4% in 2016 and 3.6% in 2017.

Among the more conservative market projections are:

McKinsey & Company establishes in a 60-page research report - Diminishing Returns: Why Investors May Need to Lower Their Expectations - why total returns from both stocks and bonds in the United States and Western Europe are likely to be substantially lower over the next 20 years than they were over the past three decades.

BlackRock, the world's largest asset manager with over $4.77 trillion in assets under management, anticipates a low-return world, with future market returns likely to be lower than in recent history; volatility increasing and the effectiveness of monetary policy to drive asset values waning.

Goldman Sachs new report Flat is the new up anticipates a potential 6-month return of 0.1% for the S&P 500 through the remainder of 2016, resulting in a return of 2.74% for the whole year. From July 1, 2016 through June 30, 2017 the firms analysts are forecasting a 1.24% return for the S&P 500.

Warren Buffett offers the caution, Corporate earnings have never been better. As a return on tangible equity, American business has never had it so good: Profits as a percentage of GDP, profit margins up and down the line, business has been very, very good ... I don't see them jumping a lot from this level (emphasis added).

John Hussman, mutual-fund manager and president of Hussman Investment Trust, maintains investors shouldnt expect stocks to gain much more than 1.2% annually for the next decade because the market is fully valued compared with corporate output. Years of yield-seeking speculation have already driven stock valuations to levels where prospective 10- to 12-year total returns for the S&P 500 are likely to be no different than the near-zero yields available on Treasury securities.

Will the low-return forecasts become reality? Maybe. Maybe not. The future has a way of surprising us. But the concerns presented by the firms and individuals are real and they need to be considered as we plan for retirement and other financial goals. It may be prudent to increase your savings or scale back on retirement plans. You may want to consider alternative investments or different investment approaches. An active management approach that strives to reduce losses in market downturns, has the potential to leverage returns when the market turns back up and benefit from short-term trends.

Investing works best when you take a flexible approach and look for opportunities. This is one reason why we find the trend toward passive investing in index funds distressing. Every market presents opportunities for profit whether through targeting specific sectors, countries or companies, avoiding drawdowns to capture the benefit of rebounds or even inverse investing. By being open to opportunities, we have the ability to look beyond the overall market return and take advantage of those opportunities.

Japan is a poster child for low to negative interest rates, minimal economic growth, an aging population and a stock market that has gone nowhere in 20 years. But could one have invested successfully in the market? In a June 13, 2016 article in the Wall Street Journal, author Ken Brown says yes, but it would take an active investment approach. Low growth has not meant low volatility for the Japanese market, which has fallen by more than 2/3s twice in the last 20 years, only to gain more than 100% in the subsequent market upswing. Successfully trade those moves and opportunity opens up. With that said, all investing carries risk and there can be no guarantee that an active strategy will successfully capitalize on market volatility. There is always the potential for loss as well as gain.

TOP

Passing on Assets without a Will

The death of a celebrity always brings out articles reflecting on their lives, successes and mistakes, and the effect they had on others. But within the investment advisor realm, articles almost always revolve around the effectiveness of their estate planning and in particular

the will.

Wills get a lot of attention because once they go through probate court (a process that can take months), they become public documents. A copy is given along with a listing of all the assets of the estate to all the heirs and beneficiaries as well as the estates executor, lawyer, accountant and even the IRS.

Thats a lot of disclosure that you may not want to happen. In which case, its time to look at how to die without having the majority of your assets and how you choose to dispose of them disclosed to the public or for that matter, family members and other potential heirs.

Pay on Death and Transfer on Death Accounts

You can convert your bank accounts, retirement accounts and even brokerage accounts to payable on death (POD) or transfer on death (TOD) by completing your financial institutions beneficiary designation form. These assets pass directly to the named beneficiaries on your death, are not subject to probate, and stay out of the public eye. Some states even allow transfer on death designations for vehicle registrations and real estate deeds. Beneficiary designations take precedence over any language in your will, however, so make certain and keep these designations up to date.

Money inherited through a POD or TOD account is included in the calculation of estate taxes and may be subject to creditor claims as well as estate taxes.

Joint Accounts

Certain forms of joint ownership of a property also allow assets to pass directly to the surviving owner(s). These include joint tenancy with right of survivorship and "tenants by entirety" accounts (applicable only for married couples, or in a few states, by same-sex partners who have registered with the state). In community property states, community property automatically passes directly to ones spouse. Here again, while the property avoids probate court, it may not avoid the claims of creditors or estate taxes.

Living Trusts

A living trust is a trust you set up and administer while you are alive, keeping full control over all property held in trust. The big advantage to making a living trust is that property left through the trust doesn't have to go through probate court and there is no disclosure of the terms of the trust. Upon your death, your executor distributes the assets to your beneficiaries according to the trust provisions. The biggest mistake people make with living trusts is failing to transfer assets into the trust before they die.

Living trusts are still vulnerable to creditor claims and are included in estate tax calculations.

An Irrevocable Trust is not included in your estates value for tax purposes and properly set up, will protect assets from creditors claims, but the assets you place in the trust cannot be retrieved. Once transferred, they belong to the trust.

So why bother with a will?

A will is an essential back-up device for property that isnt included in beneficiary designations, joint ownership or transferred to a trust. Your will can also be used to establish payment of creditors and estate taxes first from property covered by the will. Without a will, any property that goes into probate will go to your closest relatives in an order determined by state law.

Keep in mind that this a very limited discussion of estates and inheritance and tax impacts of dying and is not intended as legal advice. Make certain and talk to a qualified estate planner to assure that your assets go where you intend and taxes are minimized after your death.

TOP

Sometimes, when investing seems to get entirely too dry and calculating, it helps to toss in a few metaphors to lighten the conversation.

Dead cat bounces occur after an investment drops substantially and then has a moderate upward move, only to fall again. The visual that comes to mind at the words, pretty much describes the performance of the investment.

Black swans are those rare unforeseen events that send the market into a tailspin. The term originated in Europe where all swans were white. With the exploration of Australia, came the discovery that black swans can be relatively common.

Castles in the sky refers to periods of extreme overvaluation in the markets. While you might want to avoid castles, bottom fishing among the oversold stocks of a market drop can be profitable.

Witching hours happen during the final hour of trading on a Friday when stock index futures, single stock futures, stock index options, and stock options all expire and anything can happen. This occurs on the third Friday in March, June, September, and December.

Unicorns are those mythical privately held companies that quickly reach $1 billion in revenue and are considering going public. Its hard to be sure whether they are real or not.

The rubber band effect is the tendency of the market to bounce back right away after a large sell-off in the market, often as a result of computerized trading.

Black typically indicates a very bad, very down day in the market as in Black Monday (October 19, 1987) or Black Tuesday (October 29, 1929).

TOP

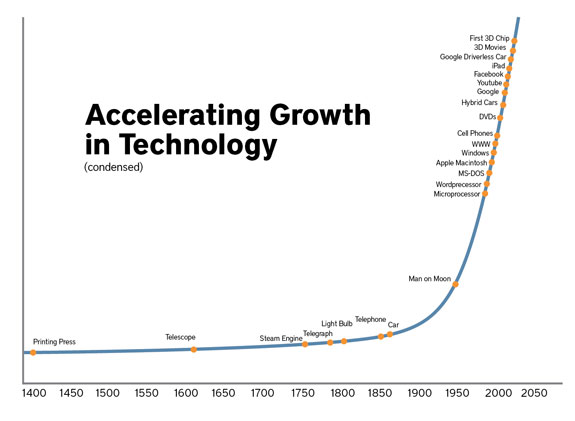

Outliving the Doomsayers

the One Constant is Change

In 1798, Thomas Robert Malthus predicted a grim future for mankind maintaining that population would increase geometrically, doubling every 25 years but food production would grow arithmetically (rising as 1,2,3,4, etc.). The result would be famine and starvation, unless populations were controlled. Fortunately, he proved spectacularly wrong.

Malthus was not the first, nor will he be the last to overlook the power of human ingenuity and technology to change the course of history. What is amazing is the accelerating pace of world-changing innovation. So before you accept any forecasts of impending catastrophe take a moment to consider how often the experts have failed to anticipate new technologies and how fast the world can change.

Source: The Internet of Things and Transportation, July 17, 2013 blog by Brent Merswolke. https://miovision.com/

Some spectacularly inaccurate predictions by the experts of their day include:

1830: "Rail travel at high speed is not possible because passengers, unable to breathe, would die of asphyxia." Dr. Dionysius Lardner

1876: This telephone has too many shortcomings to be seriously considered as a means of communication. William Orton, President of Western Union.

1903: The horse is here to stay but the automobile is only a novelty a fad. President of the Michigan Savings Bank advising Henry Fords lawyer, Horace Rackham, not to invest in the Ford Motor Company.

1921: The wireless music box has no imaginable commercial value. Who would pay for a message sent to no one in particular? Associates of David Sarnoff responding to the latter's call for investment in the radio.

1936: A rocket will never be able to leave the Earths atmosphere. New York Times

1943: "I think there is a world market for maybe five computers." Thomas Watson, chairman of IBM.

1946: Television wont be able to hold on to any market it captures after the first six months. People will soon get tired of staring at a plywood box every night. Darryl Zanuck, 20th Century Fox.

1959: "The world potential market for copying machines is 5,000 at most," IBM told the eventual founders of Xerox.

1961: There is practically no chance communications space satellites will be used to provide better telephone, telegraph, television or radio service inside the United States. T.A.M. Craven, Federal Communications Commission (FCC) commissioner.

1966: Remote shopping, while entirely feasible, will flop. Time Magazines rationale for saying remote shopping would flop: Because women like to get out of the house, like to handle merchandise, like to be able to change their minds."

1977: There is no reason anyone would want a computer in their home. - Ken Olson, president Digital Equipment Corp.

1981: Cellular phones will absolutely not replace local wire systems. Marty Cooper, inventor.

1981: "No one will need more than 637KB of memory for a personal computer. 640KB ought to be enough for anybody." - Bill Gates, founder of Microsoft

1992: The idea of a personal communicator in every pocket is a "pipe dream driven by greed," - Andy Grove, then CEO of Intel.

1995: I predict the Internet will soon go spectacularly supernova and in 1996 catastrophically collapse. Robert Metcalfe, founder of 3Com.

2005: Theres just not that many videos I want to watch. Steve Chen, CTO and co-founder of YouTube, expressing concerns about his companys long term viability.

2006: Everyones always asking me when Apple will come out with a cell phone. My answer is, Probably never. David Pogue, The New York Times.

2007: Theres no chance that the iPhone is going to get any significant market share. Steve Ballmer, Microsoft CEO.

2009: "I am 100 percent sure the U.S. will go into hyperinflation." Marc Farber, PhD

TOP