In Anticipation of Higher Interest Rates

On Jan. 20, 2017, Donald Trump will be sworn in as the 45th President of the United States. Two months prior, Wall Street began betting that interest rates are about to rise, with bets on U.S. short-term rates at $2.1 trillion. Expectations for a Trump presidency include a Federal Reserve that will be under pressure to raise interest rates in a way that hasn't been seen for more than a decade.

What will rising interest rates mean for investors?

There are simple answers and more complex "it depends" answers to the impact of increasing interest rates. The "it depends" answers reflect the uncertainty that surrounds interest rates and the economy. (1) Interest rates have never been held artificially low for such an extended time. (2) Abnormally low interest rates for eight years have been interwoven into the fabric of our economy in ways that may not be understood until they increase. (3) The economy will play an important part in the impact. While increased interest rates would be expected to lower spending, if inflation or a growing economy generates spending, the real interest rate (the nominal rate minus expected inflation) could remain relatively steady.

On the lines of historical expectations, increasing interest rates are typically a negative for stock prices. That may not hold true this time. Stock markets have reacted favorably to a Trump presidency, anticipating increased economic growth and higher inflation. Higher interest rates also indicate a return to normalcy after eight years of Federal Reserve funds rates at 0 and near 0%, which may give greater confidence to consumers and businesses.

Bonds are different. When interest rates rise, investment-grade bond prices fall. Bond funds will reflect this reality in lower prices. How much lower will depend upon how much interest rates change. Held to maturity, bonds will still have the same cash value, but investors suffer an opportunity loss when their funds are not earning market returns. New investments in bonds, however, should realize higher returns as a result of increased interest rates.

Individuals with money in a bank account should benefit from rising interest rates, provided banks actually pass the extra interest on to savers.

Pensions funds and other institutional investors will have higher return, low-risk options when investing incoming funds, which should improve their performance.

There's typically little in the way of good news for borrowers when interest rates increase. Credit card rates already have a huge gap between interest rates and the rates charged cardholders and may not see much impact. Variable rate loans could see a noticeable interest rate increase when they adjust, and the cost of new loans will increase. Longer term loans, such as 30-year mortgages, tend to be more influenced by economic expectations. If the economy improves, borrowing costs for homes and cars would be expected to increase.

The biggest negative impact of rising interest rates will hit the biggest borrowers, which are almost inevitably governments, from the federal government down to the state and local levels. The federal government has approximately $19 trillion in outstanding loan obligations on which it pays more than $432 billion a year in interest. The states have an additional $4 trillion plus in outstanding loans. Higher interest rates will take their toll when outstanding obligations are rolled into new debt offerings, or additional funds are raised through new borrowing. An improving economy with increasing tax collections could offset higher interest rates, however.

Perhaps the biggest advantage of interest rate increases will be a return to market-controlled interest rates along with normal business and market cycles. The Fed's nearly a decade-long experiment with artificially low interest rates has failed to produce expected benefits and resulted in a bloated Federal Reserve balance sheet with more than $4.4 trillion in debt-backed securities of questionable value, the consequences of which are still to come. Or to put it a bit more harshly in the words of financial analyst and author John Mauldin;

"By lowering rates to the zero bound, the Fed stacked the deck in favor of a relatively small number of people who own the vast majority of financial assets. In so doing, it created the conditions for moribund economic growth, persistent unemployment and underemployment of working-class citizens, and impoverishment of savers, and decimated fixed-rate income returns of pension funds and retirement plans for the middle class."

It's time for a return to normalcy.

Wall Street Is Betting $2.1 Trillion That U.S. Rates Will Rise, by Min Zeng, Wall Street Journal, Nov. 22, 2016

TOP

Combining Active and Fundamental Investing - Or Why We Invest the Way We Do

Investopedia defines investing as the act of committing money or capital to an endeavor (a business, project, real estate, etc.) with the expectation of obtaining an additional income or profit.

At its core, investing seeks opportunities where the addition of money can create value in excess of the original investment. With respect to publicly owned companies, the addition of money/capital occurs when the company makes a public offering, exchanging stock for money, or issues debt, promising to repay the money with interest. In the process, shares of the company or debt obligations are created that can be traded among investors.

Successful investments, Benjamin Graham and the fathers of portfolio management believed, come down to the fundamentals of the company its ability to create value as a result of the right products or services, good management and financial capacity. As the company grows, so does the value of its investors' capital. Investors profit through (1) dividends from the company and (2) more valuable stock, or in the case of bonds, (3) a predictable, competitive return on their loan.

The fundamental value of the underlying company is the logic behind a buy-and-hold investment approach. One buys stock or bonds of a good company with good growth prospects and then lets time and compounding take effect. Diversifying one's investments among different companies and industries reduces the risk that the faltering of one company could destroy a portfolio. For many years, active mutual funds were used to diversify one's investments among multiple companies selected by the portfolio manager. While index funds have replaced the active mutual fund in many portfolios, the structure of the index often selects the biggest and best of an industry segment.

But picking good and even great companies still leaves the investor vulnerable to the extremes of market volatility.

"The market has a way of punishing those who forget that investing is above all else cyclical, and that extrapolating recent results into the future is not only dangerous, it is often 180 degrees from what happens next." Rob Isbitts

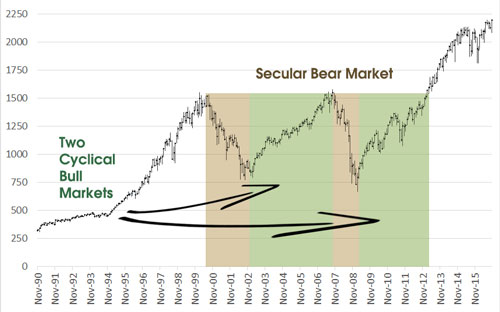

Financial markets in the U.S. have historically moved through overlapping cycles. Secular markets are long term trends lasting up to 30 years with bull and bear market phases taking from 10 to 20 years. Within the longer trend, cyclical markets occur, generally lasting around four years with bull and bear market phases taking some one to three years. Within these overlapping cycles, asset classes follow distinct cycles reflecting business and seasonal cycles.

S&P 500 Secular and Cyclical Markets - 1990-2016

Data: Yahoo Finance Weekly S&P 500 High Low Close

Buy-and-hold investors will look at the chart above and conclude that regardless of how far the market has dropped in the past, it has always recovered, returning to prior highs. The problem with this approach is that the investor can never know for sure when a bear market will occur, how long or deep it will be, or whether circumstances will arise that will necessitate selling their investments. This is the true risk of investing - will your money be there when you need it?

The cost of a bear market is more than monetary. It also shakes the confidence of investors and makes them reluctant to trust their money to the volatility of the market. It creates personal strains, stresses relationships and causes individuals to forego opportunities, postpone retirements and more.

Active investment management adds a layer of risk management to the portfolio. By monitoring markets through trend and technical analysis, we seek to determine where the market is within its cycles and position portfolios to take advantage of uptrends and reduce exposure during downtrends. While not every trade will be successful, any time we can reduce losses to market downturns, we gain leverage to potentially profit when the market recovers.

Will active management outperform a buy-and-hold position? Not necessarily over a specific period, but properly implemented it should reduce volatility, minimize losses in down markets and provide an emotionally smoother ride. Equally important, by minimizing drawdowns, the portfolio is better able to accommodate withdrawals without destroying the ability of the portfolio to recover from bear markets.

One story often used to emphasize the important of risk management is that of Abraham Wald, who was assigned damage assessments to aircraft that returned from service over Germany during World War II to determine which areas of the aircraft structure should be better protected. He made a totally unconventional assessment: Do not focus on the areas that sustained the most damage. The heavily damaged areas did not contribute to the loss of the aircraft. Instead focus on essential sections that came back relatively undamaged, such as the engines. Protect essential assets from destruction, such as large losses (drawdown), and the investor will live to invest again.

Naturally there can be no guarantee that an active investment approach will be successful. But, our track records show its advantages during past market downturns. Past performance is not a guarantee of future returns, but ignoring the market's cyclical patterns can be a guarantee of disaster.

TOP

"To be a successful investor over the long run, you must adapt to the belief that you cannot predict the market. You must use tools that remove your emotions from the decision-making process." Greg Morris, Technical Analyst and Author

One of the most important and hardest lessons for an investor to learn is to distinguish noise from information. With a proliferation of news sources from newspapers and broadcast media to financial publications, blogs, and social platforms, we are constantly bombarded with vast quantities of diverse market and economic information. The current emphasis on "content" marketing is adding to the over saturation with every financial professional contributing his daily or weekly wisdom to the overflow. The truth is very little of this information is useful when it comes to making investment decisions.

Media "experts" have a very poor track record of calling market direction. Because "bad news sells," the media's focus is overwhelming on doom and gloom. On election day 2016, the U.S. stock market fell 5% sparked purely by fears fed by media noise. Investors who bought into the noise missed the market's subsequent run to new highs.

The market trend is the truth that merits our attention. The noise distracts us from the truth and replaces a systematic approach to the markets with emotion.

TOP

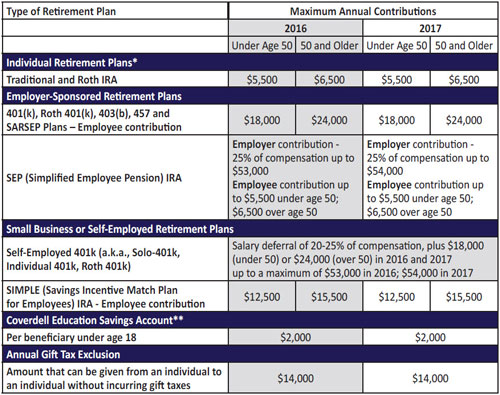

Little Has Changed in Retirement Account Contribution Limits

Retirement account contribution limits remain the same for 2017 with minimal adjustments in income limits for various account types. Remember to fully fund your account(s) for 2016 by April 15th and start funding your 2017 contributions as soon as possible to take advantage of compounding.

* The income limit for taking a full deduction for contributions to a traditional IRA while participating in a workplace retirement will increase by $1,000 for singles, from $61,000 in 2016 to $62,000 in 2017, and for married filing jointly, from $98,000 in 2016 to $99,000 in 2017. The deduction completely phases out when income goes above $72,000 for singles and $119,000 for married filing jointly, an increase by $1,000.em>

** Generally, any individual (including the beneficiary) whose modified adjusted gross income for the year is less than $110,000 ($220,000 in the case of a joint return) can contribute to a Coverdell ESA.

TOP

The Improbable Success of Seasonality Trading

When it comes to active investment strategies, one of the most fascinating – if simply because it worked for many years – is seasonality trading. Seasonality trading is based on the premise that there are good days and bad days to be invested and these days can be identified by looking at historical patterns.

The Halloween Indicator is based on the historical tendency for the stock market to produce almost all of its net returns between Halloween and the May Day (a variation of sell in May and go away). The holiday effect reflects the historical tendency for stocks to rise in the two or three trading days before a market holiday, such as the 4th of July or Christmas. The five trading days prior to St. Patrick's Day have historically proven a good time to be invested. Stocks also tend to perform better during the middle of the month.

How can such simple systems work? Wharton University Professor Donald Keim asked the same question and confirmed that there are distinct calendar-based patterns to how stocks trade. Some of the factors that may contribute to this are the timing of periodic retirement plan contributions, tax-loss selling, and short-term traders' reluctance to be exposed to stocks over a long holiday weekend.

Gerald Appel, a professional money manager, former practicing psychoanalyst, and an award-winning photographer, backtested the Halloween indicator over a half century to find it held true with amazing accuracy. Naturally, there were those exceptional years where the market reported gains or losses outside of the six months. In response, Appel developed his MACD (Moving Average Convergence-Divergence) system to signal when it might make sense to move into the market in advance of November 1st or out before May 1st.

In the early 1970s, Norman Fosback came out with his Seasonality Trading System, which was later dubbed by Mark Hulbert as the best market timing system he had encountered in years of tracking active managers. The only thing an investor needed to know was what day of the month it was.

In "Timing System Gone, Not Forgotten" from 2003, Mark Hulbert listed Norman Fosback's past timing system rules:

- Buy at the close of the third-to-last trading of each month, and sell at the close of the fifth trading session of the following month.

- Buy at the close of the third-to-last trading day prior to exchange holidays, and sell at the close of the last trading day before a holiday.

- Exceptions: If the holiday falls on a Thursday, sell at Friday's close rather than Wednesday's. Also, if the last day before a holiday is the first trading day of the week, don't sell until the day after the holiday. Finally, never sell on the first trading day after options expire; instead wait an extra day.

Naturally there are drawbacks. Fosback's system requires a lot of trading and trading costs must be kept to a minimum to avoid eating away potential gains. Popularity of the system at its height eroded its potential to produce gains due to a phenomenon known as the "crowded trade." Not every trade will be profitable.

To use seasonality systems over the long run, the investor needs to have the confidence to stick with it and overcome the psychological difficulty of spending a substantial time in cash when the market may be making new gains.

Even the most accurate seasonality trend will always be vulnerable to extreme market action, however. Trading based on the day of the month can't protect a portfolio from losses or assure gains. But it is an interesting look at how human behavior follows patterns over the years.